採用情報

採用情報

グローバル投資プラットフォーム

グローバル投資プラットフォーム SHARE

SHARE

LANGUAGE

LANGUAGE CONTACT US

CONTACT USNewsletter of FCG Group.

Newsletter of FCG Group.

Wednesday July 3rd, 2024Vietnam

TAX BULLETIN June 2024

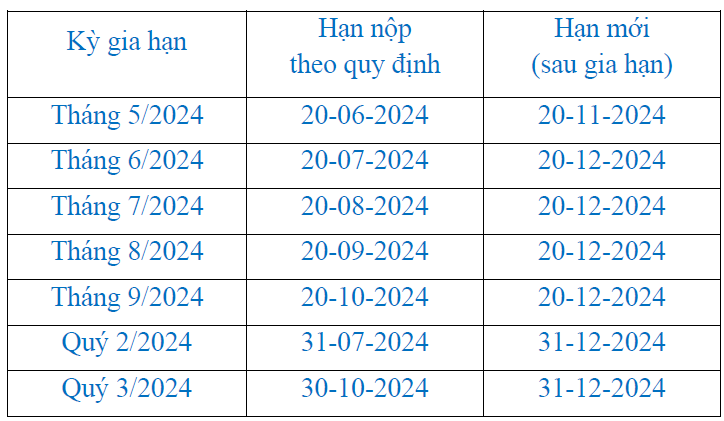

1. Government’s Decree on extension of tax payment deadlines for 2024

The Government issued the Decree No. 64/2024/ND-CP dated 17th June 2024 on extension of deadlines for payment of Value-added tax, Corporate income tax, Personal income tax, and Land rental in 2024.

➢ Value Added Tax (except for VAT at import stage):

➢ Corporate Income Tax: a three-month extension for payment of corporate income tax payable of the second quarter will be applied.

➢ Personal Income Tax: Payment of PIT payable in 2024 by household and individual business shall be deferred to no later than 30th December 2024.

➢ Land rental: Payment of 50 percent of land rental payable in 2024 (land rental payable of the 2nd period) shall be extended by two months.

The Decree takes effect from 17th June to 31st December 2024.

2. Continue 2% VAT cut for second half of 2024

Following the Tax Bulletin of May 2024, we update the release of regulation on 2% VAT reduction for the last 6 months of the year as follows: On 30th June 2024, the Government issued Decree No. 72/2024/ND-CP regulating VAT reduction according to Resolution No. 142/2024/QH15 dated 29th June 2024 of the National Assembly. In general, VAT reduction policy applied from 1st July to 31st December 2024 according to Decree No. 72/2024/ND-CP remains the same and inheriting the provisions of Decree No. 94/2023 /ND-CP. There are no changes in goods and services being subject to VAT reduction, reduction rate and invoicing requirements in comparison with the first 6 months of 2024. However, companies are required to declare goods and services eligible for VAT reduction by using the new Form No. 01 specified in Appendix IV of the Decree No. 72/2024/ND-CP to attach with the VAT return.

3. Notification of temporary suspension on exit will be publicized on the website of the Tax Office (Official Letter No. 2477/TCT-QLN dated 10th June 2024 of General Department of Taxation)

To facilitate taxpayers to research information, the General Department of Taxation requests the Provincial Tax Departments and the Large Enterprise Tax Department to summarize and review to ensure all exit suspension notices, exit-suspension extension notices, and exit-suspension cancellation notices are fully publicized on the website of the Tax Office.

4. Invoices issuance for services entitled to and not entitled to VAT reduction (Official Letter No. 2363/CTHYE-TTHT dated 11th June 2024 of Hung Yen Tax Department)

If the company provides services to customers, which include both services subject to and not subject to VAT reduction, and it is not possible to determine the tax rate for each service component:

– An invoice must be issued with the highest tax rate of 10% applicable to these services.

– The buyer can use this invoice to claim for input VAT credit and request a VAT refund (if applicable).

5. Foreign contractor tax on exported goods re-processed overseas (Official letter No. 12264/CTBDU-TTHT dated 9th May 2024 of Binh Duong Tax Department)

The Company exported goods to a client overseas; however, due to not meeting requirements of product quality in accordance with a signed trading contract, the Company had to hire another foreign entity to reprocess such exported goods. In this case, the reprocessing activity is provided and consumed outside Vietnam, and therefore income derived by the foreign entity from reprocessing the exported goods is not subject to foreign contractor tax.

6. Tax policy applied to loan interests (Official Letter No. 27296/CTHN-TTHT dated 10th May 2024 of Hanoi Tax Department)

➢ In case a parent company provides loans for its subsidiary companies without interest (0% tax rate), then this will be in-scope of related party transactions regulated under Decree No. 132/2020/ND-CP. Accordingly, the company shall adjust level of price, profit margin of the provision of loan transaction as stipulated under Clause 1, Article 8, Decree No. 132/2020/ND-CP in order to declare and calculate CIT.

➢ With regard to the activity of irregular loan provision of the company (which is not a financial institution), if the loan provider does not calculate interests or calculate interests with an interest rate lower than the normal interest rate applied in the loans with the same lending term, lending scale in the market, it may subject to tax imposition as regulated under clause 1, Article 50 of the Law on Tax administration No. 38/2019/QH14.

➢ If the company has loan interests which are converted to capital contributions by the company’s capital contributor, the individual/organization who transfers the capital contributions has to pay PIT/CIT upon clause 4, Article 2, Circular No. 111/2013/TT-BTC and Article 14, Circular No. 78/2014/TT-BTC.

【PDF】Tax bulletin_June 2024_EN

BẢN TIN THUẾ Tháng 6 năm 2024

1. Chính phủ ban Nghị định về gia hạn thời hạn nộp thuế năm 2024

Ngày 17/6/2024, Chính phủ đã ban hành Nghị định 64/2024/NĐ-CP vể việc gia hạn thời hạn nộp thuế Giá trị gia tăng, thuế Thu nhập doanh nghiệp, Thuế thu nhập cá nhân và tiền thuê đất trong năm 2024.

➢ Thuế GTGT (trừ thuế GTGT khâu nhập khẩu):

➢ Thuế TNDN: gia hạn 3 tháng thời hạn nộp thuế đối với số thuế TNDN tạm nộp của quý II kỳ tính thuế TNDN năm 2024.

➢ Thuế TNCN: Hộ kinh doanh, cá nhân kinh doanh được gia hạn thời hạn nộp thuế chậm nhất là ngày 30/12/2024.

➢ Tiền thuê đất: Gia hạn 2 tháng thời hạn nộp tiền thuê đất đối với 50% số tiền thuê đất phát sinh phải nộp năm 2024 (số phải nộp kỳ thứ hai năm 2024).

Nghị định này có hiệu lực từ ngày 17/6/2024 đến hết ngày 31/12/2024.

2. Tiếp tục áp dụng giảm thuế GTGT 2% cho 6 tháng cuối năm 2024

Tiếp theo Bản tin thuế Tháng 5, chúng tôi xin cập nhật về việc ban hành quy định giảm thuế GTGT 2% cho 6 tháng cuối năm như sau: Ngày 30/6/2024, Chính phủ ban hành Nghị định 72/2024/NĐ-CP quy định chính sách giảm thuế giá trị gia tăng theo Nghị quyết 142/2024/QH15 ngày 29/6/2024 của Quốc hội. Nhìn chung, các nội dung thực hiện giảm thuế GTGT từ ngày 01/7/2024 đến hết ngày 31/12/2024 theo Nghị định 72/2024/NĐ-CP vẫn giữ nguyên, kế thừa quy định tại Nghị định 94/2023/NĐ-CP. Đối tượng, mức giảm và cách ghi hóa đơn không thay đổi so với 06 tháng đầu năm 2024. Tuy nhiên, các doanh nghiệp cần thực hiện kê khai các hàng hóa, dịch vụ được giảm thuế GTGT theo Mẫu số 01 mới quy định tại Phụ lục IV ban hành kèm theo Nghị định 72/2024/NĐ-CP cùng với Tờ khai thuế GTGT.

3. Thông báo tạm hoãn xuất cảnh được đăng tải trên trang thông tin điện tử của Tổng cục Thuế và Cục Thuế địa phương (Công văn số 2477/TCT-QLN ngày 10/06/2024 của Tổng cục Thuế)

Để tạo điều kiện thuận lợi cho người nộp thuế tra cứu thông tin, Tổng cục Thuế đề nghị Cục Thuế các tỉnh, thành phố trực thuộc Trung ương, Cục Thuế Doanh nghiệp lớn triển khai thực hiện tổng hợp, rà soát lại để đảm bảo toàn bộ các Thông báo tạm hoãn xuất cảnh, Thông báo gia hạn tạm hoãn xuất cảnh, Thông báo hủy bỏ tạm hoãn xuất cảnh được đăng tải đầy đủ trên trang thông tin điện tử của Cục Thuế.

4. Lập hóa đơn khi bao gồm cả dịch vụ được giảm thuế GTGT và không được giảm thuế GTGT (Công văn số 2363/CTHYE-TTHT ngày 11/06/2024 của Cục Thuế Tỉnh Hưng Yên)

Trường hợp công ty thực hiện các dịch vụ được giảm thuế và không được giảm thuế GTGT, nếu không xác định được theo từng mức thuế suất thì:

– Công ty phải lập hóa đơn theo mức thuế suất cao nhất của các dịch vụ trên là 10%.

– Người mua được sử dụng hóa đơn trên làm căn cứ khấu trừ thuế GTGT đầu vào và đề nghị hoàn thuế GTGT (nếu có).

5. Hướng dẫn thuế nhà thầu nước ngoài đối với hàng hóa gia công lại tại nước ngoài (Công văn số 12264/CTBDU-TTHT ngày 9/5/2024 của Cục thuế Tỉnh Bình Dương)

Công ty xuất khẩu hàng hóa, giao cho khách hàng ở nước ngoài, nhưng do hàng hóa không đạt yêu cầu chất lượng theo hợp đồng mua bán đã ký nên Công ty phải thuê tổ chức khác gia công chế biến lại. Trong trường hợp này, do hoạt động gia công này được cung cấp và tiêu dùng ngoài Việt Nam nên thu nhập mà tổ chức nước ngoài nhận được không thuộc đối tượng chịu thuế nhà thầu.

6. Chính sách thuế đối với khoản lãi vay (Công văn số 27296/CTHN-TTHT ngày 10/5/2024 của Cục Thuế Thành phố Hà Nội)

➢ Trường hợp công ty mẹ cho công ty con vay với lãi suất 0% (không tính lãi) thì thuộc phạm vi giao dịch liên kết quy định tại Nghị định số 132/2020/NĐ-CP. Công ty phải điều chỉnh mức giá, tỷ suất lợi nhuận của giao dịch cho vay theo quy định tại Khoản 1, Điều 8, Nghị định số 132/2020/NĐ-CP để kê khai tính thuế TNDN.

➢ Đối với hoạt động cho vay không thường xuyên của các công ty (không phải tổ chức tín dụng) nếu bên cho vay không tính lãi hoặc tính với lãi suất thấp hơn lãi suất thông thường cùng kỳ hạn, quy mô trên thị trường thì thuộc trường hợp bị ấn định thuế theo quy định tại khoản 1, Điều 50, Luật Quản lý thuế số 38/2019/QH14.

➢ Trường hợp công ty có khoản lãi vay được chuyển thành vốn góp do thành viên góp vốn của công ty thực hiện chuyển nhượng phần vốn góp thì cá nhân/tổ chức chuyển nhượng phần vốn góp đó phải nộp thuế TNCN/TNDN theo quy định tại khoản 4, Điều 2, Thông tư số 111/2013/TT-BTC và Điều 14, Thông tư số 78/2014/TT-BTC.

【PDF】Tax bulletin_June 2024_VN

〈お問い合わせ先〉

Fair Consulting Vietnam Joint Stock Company

|

Hanoi Office 3F, Leadvisors Place,41A Ly Thai To St Hoan Kiem Dist., Hanoi Vietnam Tel:+84-24-3974-4839 石井 大輔 日本国公認会計士 Email: da.ishii@faircongrp.com |

Ho Chi Minh Office Unit 7, 8th Floor, Riverbank Place 3C Ton Duc Thang St, Ben Nghe Ward, District 1, Ho Chi Minh City, Vietnam Tel:+84-28-3910-1480 葉山 暁彦 日本国公認会計士 Email: ak.hayama@faircongrp.com |